Sortino ratio vs Sharpe ratio: How to choose the right risk metric

Understanding the difference between the Sortino ratio vs Sharpe ratio helps investors evaluate performance more accurately. While both measure risk-adjusted returns, they define “risk” in very different ways, which can significantly impact decision-making.

1. What the Sharpe ratio actually measures

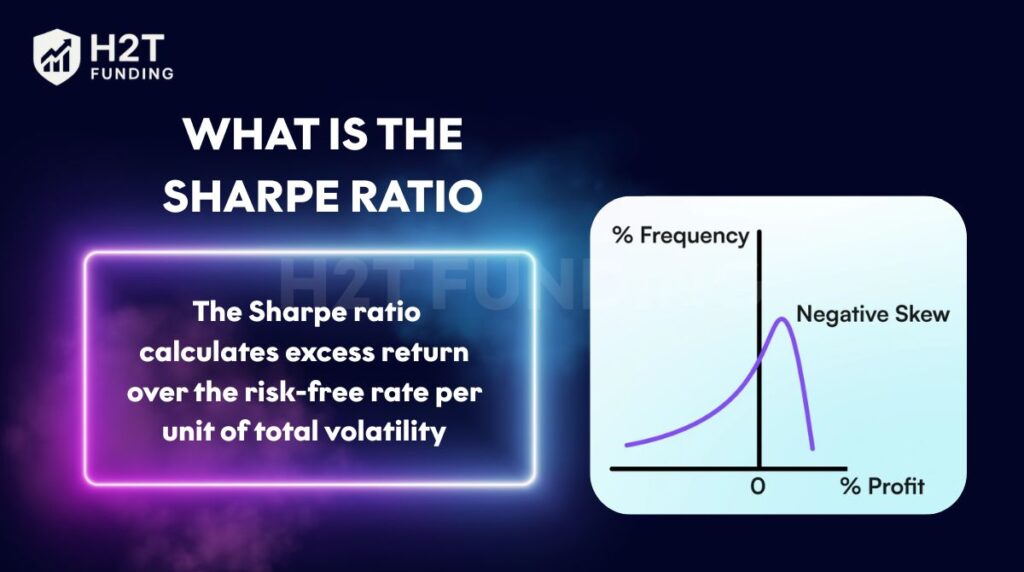

The Sharpe ratio evaluates excess return relative to total volatility. It uses standard deviation to represent risk, meaning both upward and downward price movements are treated equally. This makes the Sharpe ratio simple, widely accepted, and useful for comparing diversified portfolios with stable return distributions.

|

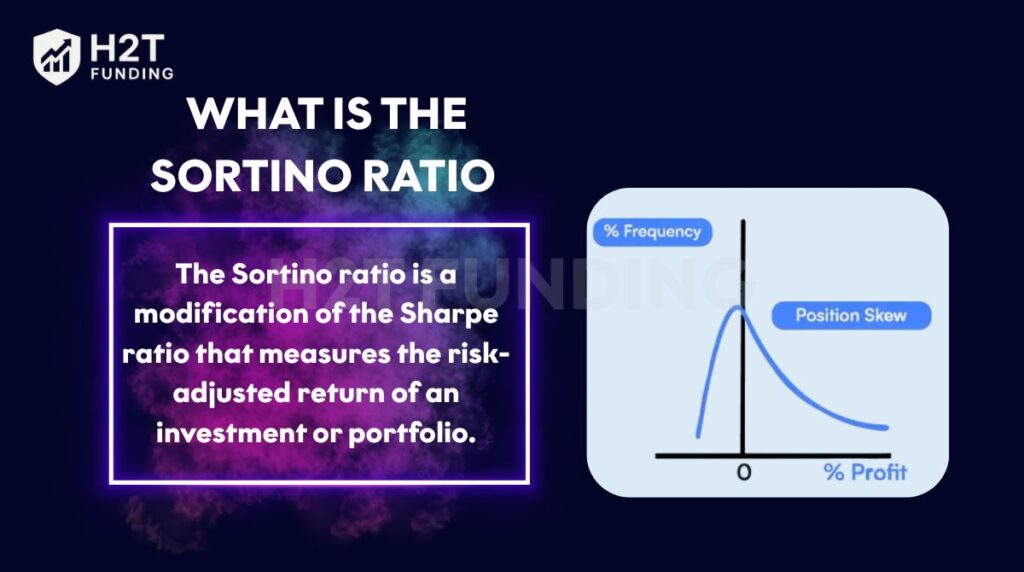

| What is the Sortino ratio? |

However, this approach can distort reality. Positive volatility, which investors generally welcome, is penalized the same way as losses.

2. Why the Sortino ratio was created

The Sortino ratio improves on the Sharpe ratio by focusing only on downside risk. Instead of total volatility, it uses downside deviation, measuring only returns that fall below a minimum acceptable return.

This makes the Sortino ratio more aligned with real investor concerns: protecting capital and avoiding losses, rather than suppressing upside potential.

3. Sortino ratio vs Sharpe ratio: key differences

The core difference lies in how risk is defined. Sharpe measures total volatility, while Sortino isolates harmful volatility. As a result, high-growth or asymmetric strategies often look weaker under Sharpe but stronger under Sortino.

|

| What is the Sharpe ratio? |

This distinction is critical when evaluating volatile assets such as growth stocks, active trading strategies, or crypto portfolios.

4. When each ratio works best

The Sharpe ratio works best for low-volatility, well-diversified portfolios where returns are relatively symmetrical. In contrast, the Sortino ratio is better suited for high-volatility or skewed strategies where downside protection matters more than smooth returns.

Using the wrong ratio can lead to incorrect conclusions about performance quality.

5. Using both ratios together

Rather than choosing one metric exclusively, many professional investors analyze both. Sharpe provides a broad performance baseline, while Sortino reveals how efficiently returns are generated relative to downside risk.

Used together, they deliver a clearer and more balanced picture of true risk-adjusted performance.

Read the full guide: https://h2tfunding.com/sortino-ratio-vs-sharpe-ratio/

#funding

#h2tfunding

#nganpham

#finance

#sortinoratiovssharperatio

#nganphamh2t

Nhận xét

Đăng nhận xét