How much should I have saved by 35 based on income? (Real benchmarks to stay on track)

If you’ve hit your mid-30s and started wondering “How much should I have in savings at 35?”, you’re not alone. For many, this is the decade when money starts to feel real — mortgages, kids, retirement, and everything in between.

While there’s no perfect number for everyone, financial experts have created helpful benchmarks to guide you. Generally, by age 35, you should aim to have around twice your annual salary saved — enough to handle short-term needs and build long-term security.

1. The 2× salary savings rule — explained

|

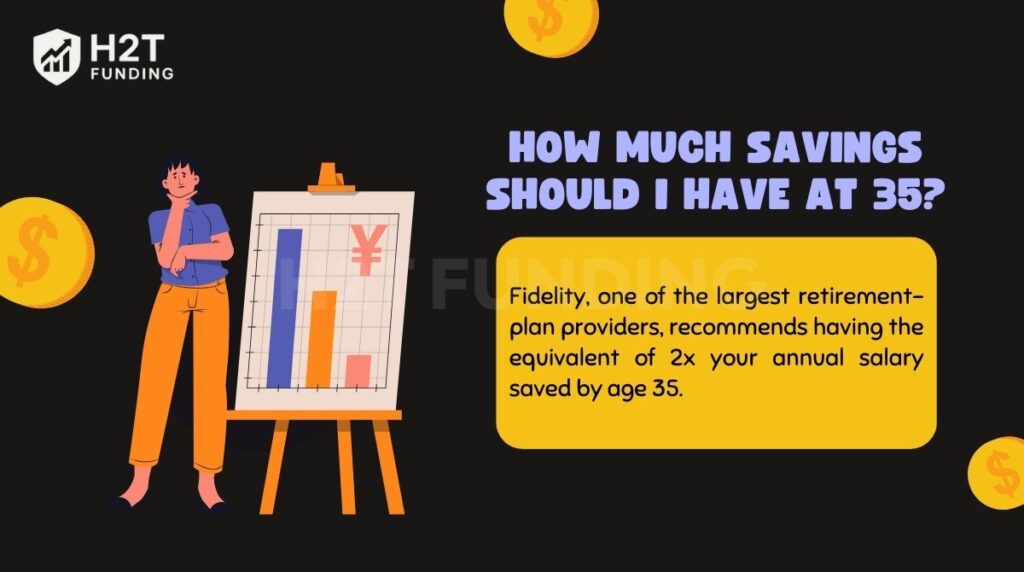

How much savings should I have at 35 |

According to Fidelity Investments, a healthy financial target by 35 is 2× your annual salary. That means:

-

$40,000 income → $80,000 saved

-

$60,000 income → $120,000 saved

-

$80,000 income → $160,000 saved

-

$100,000 income → $200,000 saved

This total includes your emergency fund, retirement accounts, and investment portfolios. It’s not about perfection — it’s about progress.

If you’re not close to that figure yet, don’t stress. The key is understanding what this number represents: financial stability, flexibility, and peace of mind.

2. Why your mid-30s are a financial turning point

At 35, you’re usually deep into your career and possibly juggling multiple priorities — family, mortgage payments, travel goals, or starting a business.

This is the age when your financial decisions compound faster than ever. Saving and investing early means your money can grow exponentially through compounding. Conversely, delaying savings too long can make catching up harder.

That’s why your 30s are often referred to as the “momentum decade.” The right steps now can set the foundation for financial freedom in your 40s and beyond.

3. Savings breakdown by income level

Let’s make this more practical. Here’s what your total savings might look like at 35, based on different income levels:

| Annual Income | Recommended Savings by 35 |

|---|---|

| $40,000 | $80,000 |

| $50,000 | $100,000 |

| $60,000 | $120,000 |

| $75,000 | $150,000 |

| $100,000 | $200,000 |

| $120,000 | $240,000 |

These are benchmarks — not judgments. Life circumstances differ. What matters most is maintaining consistent habits and aligning savings goals with your own lifestyle and priorities.

4. What to focus on saving for at 35

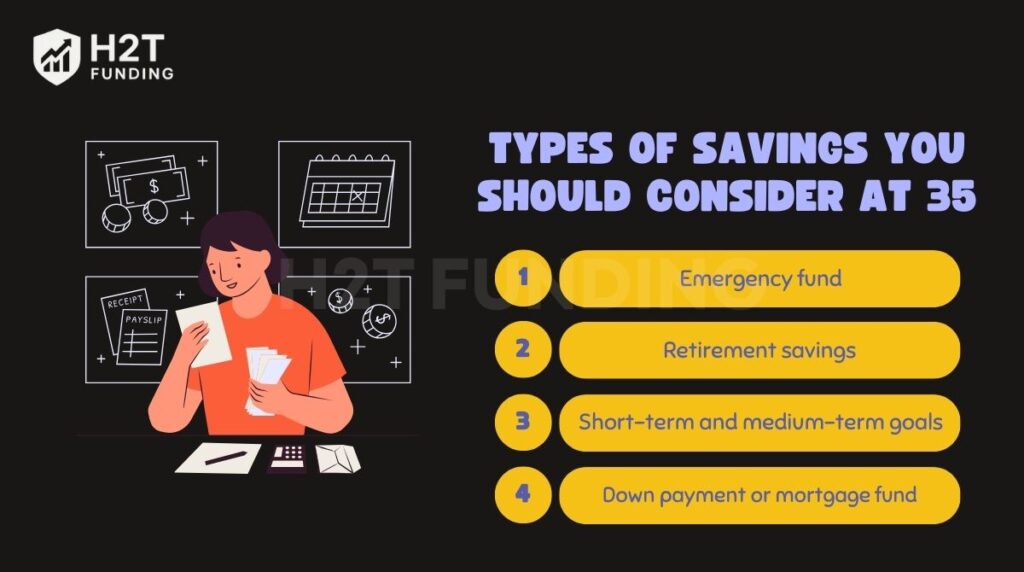

|

| Types of savings you should consider at 35 |

By this age, your money should be working across different goals, not sitting idle in one account. Here’s how to allocate your savings smartly:

-

🧭 Emergency fund: 3–6 months of living expenses.

-

💰 Retirement fund: Contribute 15–20% of your income toward a 401(k), IRA, or equivalent.

-

🏠 Down payment or home fund: Build equity instead of paying rent long-term.

-

🚀 Investment portfolio: ETFs, index funds, or real estate for long-term growth.

-

🎯 Short-term goals: Travel, education, or family plans — without dipping into long-term funds.

Diversifying your savings ensures both flexibility and security.

5. If you’re behind on savings — here’s how to catch up fast

Falling short at 35 doesn’t mean you’ve failed. You still have time to build momentum and get on track. Here’s how:

✅ Increase your savings rate — Start with 20–25% of your income and adjust upward as your salary grows.

✅ Automate everything — Set up automatic transfers to savings and investment accounts right after payday.

✅ Invest wisely — Don’t let fear stop you. Start small with index funds or ETFs and let compounding work over time.

✅ Avoid lifestyle inflation — As income grows, maintain your lifestyle and save the difference.

✅ Boost income potential — Freelance, consult, or upskill to increase your earning power.

Even if you start now, small, steady actions can make a massive difference by age 40.

6. Personal factors that influence your savings goals

Your financial reality is shaped by more than your salary. Consider these variables:

-

Debt load: Credit card, car, or student loan debt reduces how much you can save. Prioritize high-interest debt first.

-

Living costs: Big-city expenses often limit savings, so adjust expectations based on your region.

-

Family status: Kids, education costs, or supporting parents affect cash flow.

-

Career stability: Freelancers or entrepreneurs may need higher emergency savings buffers.

-

Investment comfort: More risk tolerance can mean faster growth, while conservative savers prioritize stability.

Personalizing your plan makes it sustainable — not stressful.

7. How to grow your savings faster in your 30s

Your 30s are the perfect time to build financial momentum. Try these proven strategies:

-

💸 Max out employer retirement matches — It’s free money.

-

📈 Automate investing — Consistency beats timing the market.

-

🧾 Track spending weekly — Awareness prevents overspending.

-

🪙 Reinvest earnings — Dividends or side income should go back into investments.

-

💬 Educate yourself — Financial literacy pays lifelong dividends.

When you treat saving as a non-negotiable, your future self will thank you.

8. Final takeaway

So, how much should you have in savings at 35?

Aim for about two times your annual income, but focus more on habit-building and consistency than on hitting an exact number.

Financial progress isn’t about where you start — it’s about what you do next. Every automated transfer, every extra contribution, and every smart investment moves you closer to freedom.

Your 35-year-old self is building a foundation that your 50-year-old self will be grateful for. Start today, stay consistent, and watch your wealth grow.

👉 Full article: https://h2tfunding.com/how-much-savings-should-i-have-at-35/

#funding #h2tfunding #nganpham #finance #howmuchshouldIhaveinsavingsat35 #nganphamh2t

Nhận xét

Đăng nhận xét